Think about how you’d feel if your investment dropped by 20% in a year. If that thought keeps you up at night, you might have a low-risk tolerance and should lean toward less volatile investments.

The key is to investing keep it simple. Investing is just like writing a 50K word book. Is it hard? You’re damn right. But if you break it up into 25 sessions of writing 2K words at a time, it’s not that bad.

The key word is simple. Make hard things simple and you’ll be fine.

Here are 12 simple questions you should ask yourself before making an investment decision so you don’t end up losing your hard-earned money.

1. What is my financial goal?

Clearly define what you hope to achieve with your investments. That’s the first step to all investing decisions. Are you saving for retirement, a down payment on a house, or your child’s college education? Your financial goals should guide your investment strategy.

Let’s say you’re saving for retirement. You might consider a more conservative approach with a focus on long-term growth. If you’re aiming for a down payment on a house, you might need a more aggressive strategy to grow your money faster.

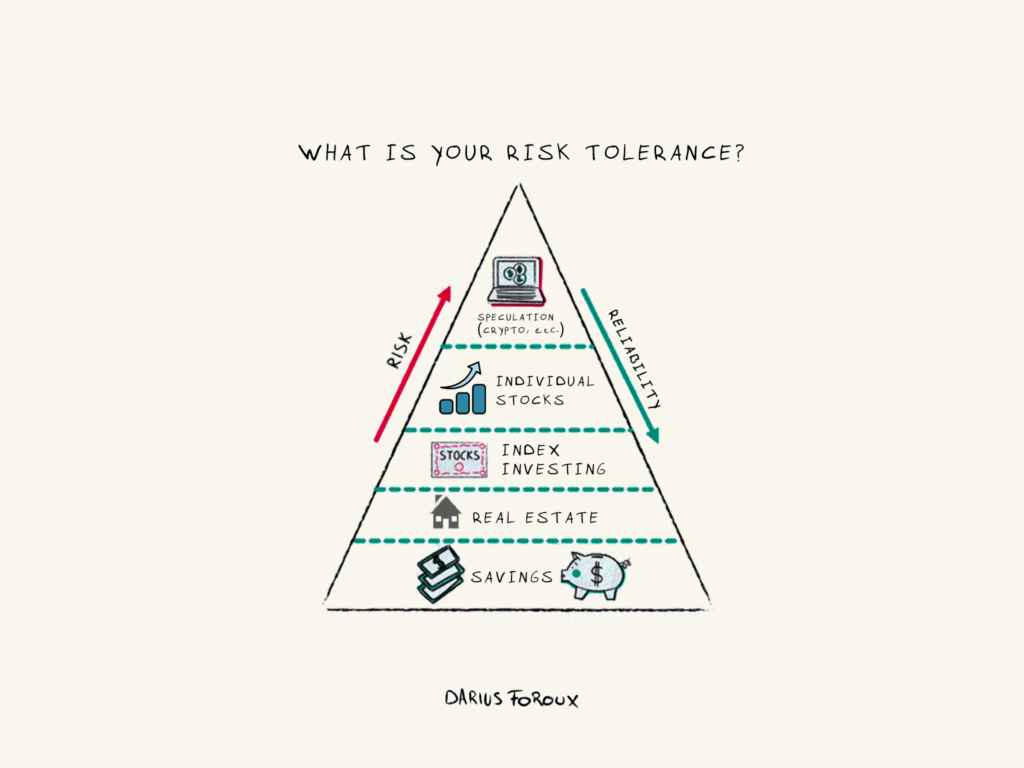

2. What is my risk tolerance?

Every investment carries some level of risk. It’s crucial to understand how much risk you’re comfortable taking on. Can you handle the potential loss if the investment doesn’t pan out within your expected time frame?

Think about how you’d feel if your investment dropped by 20% in a year. If that thought keeps you up at night, you might have a low-risk tolerance and should lean toward less volatile investments.

3. What is the time horizon for my investment?

Your investment timeline determines the kind of investments you should consider. For short-term goals (like saving for a vacation or a car), liquid investments like money market funds.

For long-term goals (like retirement), real estate and index investing generally have much higher returns.

4. Do I understand the investment?

Make sure you understand how the investment works and the factors that influence its performance. That’s crucial when it comes to investing decisions. If you can’t explain how the company makes money to a 5-year-old, you probably shouldn’t invest in it.

For example, if you’re considering investing in cryptocurrency but don’t understand blockchain technology and the nature of currencies, it’s likely not a good choice.

You don’t have to be an expert to invest. But you do need to have a good understanding of how the business works and how it profits. Otherwise, you’re just gambling money based on hype and other people’s opinions.

Investing in things you have zero knowledge about is a sure way to lose money.

5. How liquid is the investment?

Liquidity refers to how quickly an investment can be converted into cash. If there’s a chance you’ll need your money back in the short term, opt for investments with high liquidity.

Stocks and bonds are generally highly liquid as they can be sold on the market relatively easily. Real estate, on the other hand, can take much longer to convert into cash.

6. What are the costs associated with the investment?

Fees and costs can eat into your investment returns. Be sure you understand all the costs associated with the investment, including broker fees, transaction fees, and management fees.

For instance, index funds typically have lower fees than actively managed funds. Over time, even a 1% difference in fees can significantly impact your returns due to compounding. Knowing you’ll grow your wealth over time is one of the easiest investing decisions to make.

7. What are the tax implications?

Different investments have different tax implications. Consider how your investment will be taxed and how it will affect your overall financial situation.

For example, in the US, long-term capital gains (from investments held for over a year) are taxed at a lower rate than short-term gains. This could influence your decision to hold or sell an investment.

8. How does this investment fit into my overall portfolio?

Diversification is key in investing. Make sure the investment complements your existing portfolio and doesn’t expose you to unnecessary risk.

If your present portfolio is heavily weighted in tech stocks, investing in a tech ETF might expose you to unnecessary risk. Instead, consider diversifying into other sectors or asset classes.

9. What is the track record of the company or fund?

Research the performance history of the company or fund you’re considering. While past performance isn’t a guarantee of future results, it can give you an idea of the company’s stability and growth potential.

You might not count on it, but don’t expect annualized 20% returns from the S&P 500. Maybe from the Nasdaq 100. But nothing is guaranteed.

10. Who is managing the investment?

The competence and integrity of the management team can greatly influence the success of an investment. Research their track record and reputation.

In investing, people often talk about, “Betting on the jockey.” The idea is that you’re better off if you invest in a fund manager, founder, or CEO, who are the best at what they do.

If you consider picking stocks, make sure you trust the person who runs the underlying investment (in the case of companies, the CEO; in the case of funds, the fund manager). The right person will make a huge impact to your investing decisions.

11. What are the potential returns?

While it’s not possible to predict exact returns (especially in the short-term), you should have a general idea of what you can expect to earn from the investment in the long run.

For example, here are the historical returns for common asset classes: 1Source: The Measure of a Plan

12. What’s the alternative?

My gold standard of investing is the S&P 500 Index, which historically did about 10% returns a year. It’s a solid investment, but it doesn’t have an insane return.

When I look at individual stocks, bonds, or real estate, I always compare it to the S&P 500.

You might run into interesting investment opportunities, but are they better than the alternative?

Always keep it simple

Look, you don’t need to hire a financial advisor, accountant, or tax consultant when you start out. Leave that to later in your career, when you’ve built a significant portfolio.

In the first decade of your investing career, it’s all about educating yourself and making reasonable decisions. Don’t try to hit home runs.

Understand the skill of investing. The more you know, the more you will earn in the long-term.

A good understanding of what good investing looks like will pay you dividends for the rest of your life.