How do you know if you’re ready to start investing? Here’s a thought experiment to see if you have the right mindset.

Imagine you’re at a conference and you happen to sit next to the former chairman of the Nasdaq.

He proposes an investment opportunity to you with guaranteed returns of somewhere between 13% to 20%. Would you get in?

If you do, then you’re doing something “natural.” Many people base their decisions on credentials. Well, that guy was Bernie Madoff, and he made that offer to many smart investors. He had all the credentials:

- He owned legitimate businesses

- Congress often called him to testify in relevant financial matters

- He used to be the chairman of Nasdaq

Madoff took people’s money and didn’t invest it at all. He simply gives them back somewhere between 13% and 20%. Just a little bit more than the S&P500 returns, so it seemed legit. But it was a Ponzi scheme.

Madoff started his scam in the early 90s, and he wasn’t caught until 2008. Investors lost a total of over $17.5 billion.1Source: Forbes

But not everyone got swayed by Madoff. The investor Howard Marks often tells the story of how he didn’t trust the investment opportunity Madoff presented because it didn’t sound logical.

With basic knowledge of how investing and finance work, we can do the same with investment opportunities. No one can “guarantee” returns.

In this article, I share 4 things investors need to know before starting to invest. By taking the time to learn more now, you can save yourself a lot of pain in the future.

1. The difference between short-term trading and long-term investing

Before you start investing, ask yourself: “What is my investing goal?”

- Is it to build long-term wealth, with the goal of a comfortable retirement?

- Or a means to increase your income?

The former is long-term investing. The latter is short-term. Investors who look at investing as an income-generating tool invest with the mindset that they’ll pull it out in a year or two.

Short-term investors are trading stocks, buying and selling in a day, week, or month. This is fine for people who understand the stocks they’re trading. But most of us don’t have the desire to become a trader.

I don’t look at investments as a means to increase my income. That’s what my career is for. To me, investments are for building long-term wealth by using the power of compounding.

Your mindset determines your expectations. And when it comes to investing, we need to have realistic expectations.

2. Investing is a habit, not an act

Investing is a habit.

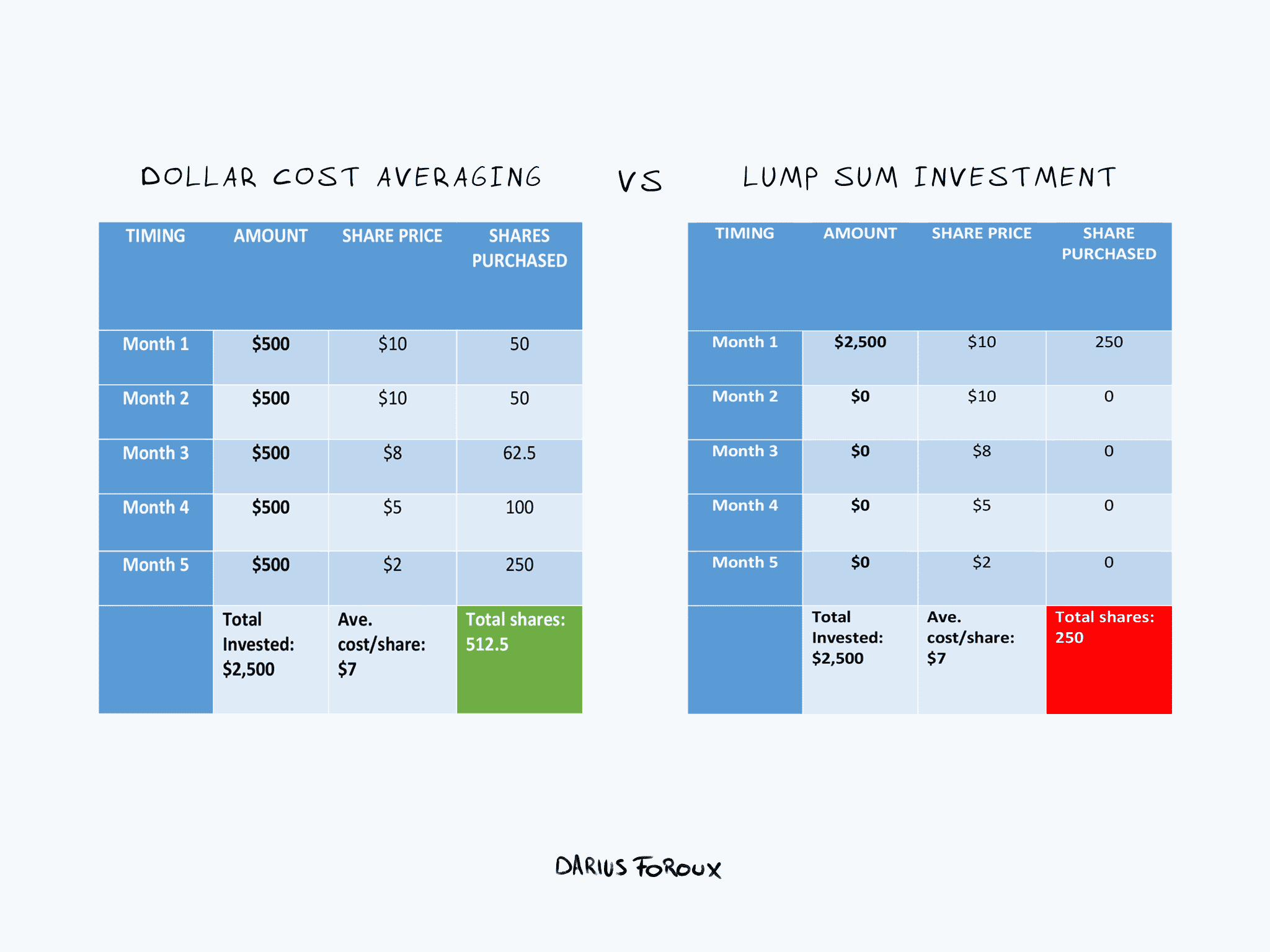

Making a one-time, lump-sum investment won’t go far. And if your investing goal is to build long-term wealth, then you’ll need a consistent investing routine.

Timing the market is difficult since share prices are volatile. Prices could be up this month, then down the next, and so forth. So instead, I apply “dollar cost averaging.” I invest a consistent percentage of my income every month, regardless of price.

This lowers the impact of market timing on my investments. It also gives me less stress.

Let’s say you’ll commit to investing $500 a month. (If you invest that amount in the S&P 500 index fund for 35 years, you can actually become a millionaire). If you apply dollar cost averaging, this is how your investments might look like in a 5-month period:

Finally, stick to an amount that’s sustainable for you. If 30% of your income is doable, then great. If not, go with 10% or 20%. It depends on how much you can realistically miss.

You might have a new kid, or buy a house, and so forth. These things will affect how much you can invest. So adjust the investment accordingly.

The important thing is to remain consistent over the long term. If you invest little today, invest more in the future. Whatever it is, stick to your investing goal every month. Your future self will thank you for it.

3. How often corrections and bear markets happen

“Market correction” and “bear market” both mean a period of decline in the stock market. But they’re not the same. By definition:

- A correction happens when the market drops at least 10% from its most recent high. This usually happens once every (roughly) 2 years. And it’s often because a major event or economic shock made investors sell more than buy.

- A bear market is a decline of 20% or more. And it lasts from a few months to an average of a little over a year. Bear markets occur every 7 years on average in recent decades. They primarily happen because of low economic growth.

Why is knowing the difference important? Because corrections happen more frequently and last shorter while bear markets can last for years, with much lower growth.

If you’re a long-term investor, you can simply stay the course. There’s no need to respond to the market. Your returns might take a hit, but in the grand scheme of things, it’s meaningless.

Long-term investors understand that in a span of 10 or 20 years, there will always be various corrections and bear markets. It’s just part of the game.

4. How you can spot get-rich-quick schemes

If an investment opportunity is too good to be true, then it probably is. We’ve all heard of it. But we can still get swayed to put our money into questionable investments.

Investing comes with two powerful emotions: Greed and fear. When we hear about an opportunity to make more money, we feel an itch. That itch is greed. When bad things happen to the economy and investors start panic-selling, that’s fear.

The key is to identify these emotions when they arrive, ignore them, and stick to our plans. I really like this quote from John Bogle, the founder of the Vanguard index fund. In his book, Stay the Course, he says:

“The winning formula for success in investing is owning the entire stock market through an index fund, and then doing nothing. Just stay the course.”

Many of the people that Bernie Madoff defrauded were professional investors. Yet, why do smart people get scammed into bad investments? That’s because emotions are involved.

Smart investing is all about managing your own emotions. You don’t let your impulses dictate your investment decision.

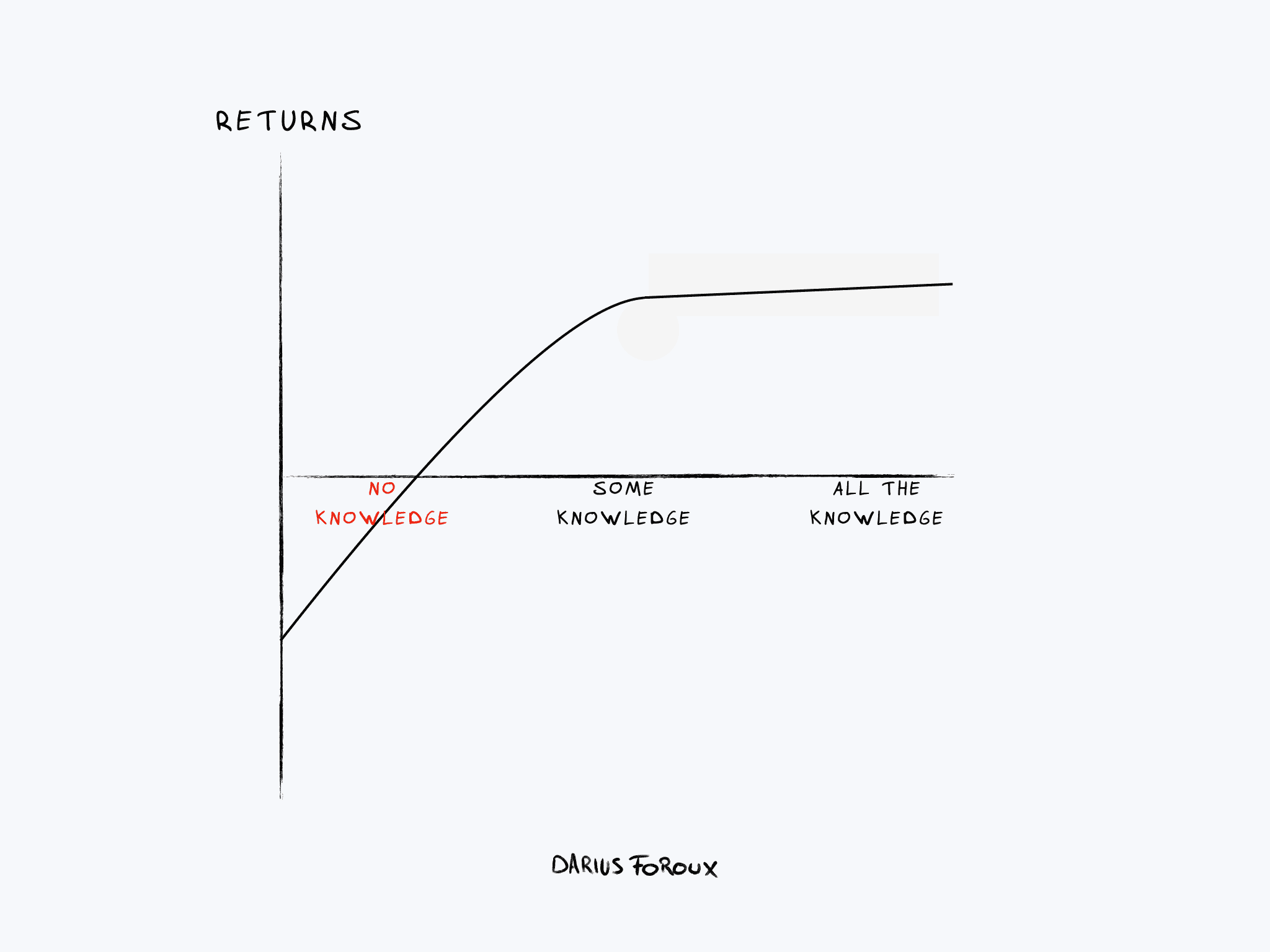

Having some knowledge vs all the knowledge

You don’t need a finance degree to start investing. But blindly going in full of uninformed expectations can lead to lost investments.

That’s why I have a very simple investing strategy. When I know the basics of investing and understand the fundamental principles of why the market acts the way it does, I have more peace of mind. I don’t easily get swayed by public opinion, the news, or armchair experts.

Likewise, we don’t need to read every book on investing and dig through every historical data. As Warren Buffett puts it:

“If past history was all that is needed to play the game of money, the richest people would be librarians.”

When you’re equipped with some knowledge, you have an edge against investors getting into the game blindly. And your returns are likely to be similar to the pros, and probably even better in most cases.