When can you buy a nice car, a month-long vacation, or even a dinner at a top-tier restaurant — while being guilt-free about the expense?

You’ll notice I use the word “when.” That’s because luxuries don’t have to be a strict buy-it-or-forget-it situation. I believe we can afford to buy most things we want in life, even those that are considerably “luxurious.”

I’ve talked about being free from money guilt if you’re a naturally frugal person. It’s best to look at luxury spending from a milestone perspective.

For example: I only bought a nice car after buying a house, owning a rental property, and having a high six-figure stock portfolio.

Before I accomplished those goals, I drove older and much cheaper cars. I didn’t bother with brands or prestige or even my childhood “dream car.”

Those things had to wait until I bought a house. For me, buying assets that are more likely to appreciate in value over time is a better way to spend rather than cars, which depreciate.

You can use this milestone-setting mindset to allow yourself to buy “something nice” guilt-free. And you can level your milestones depending on your unique financial situation.

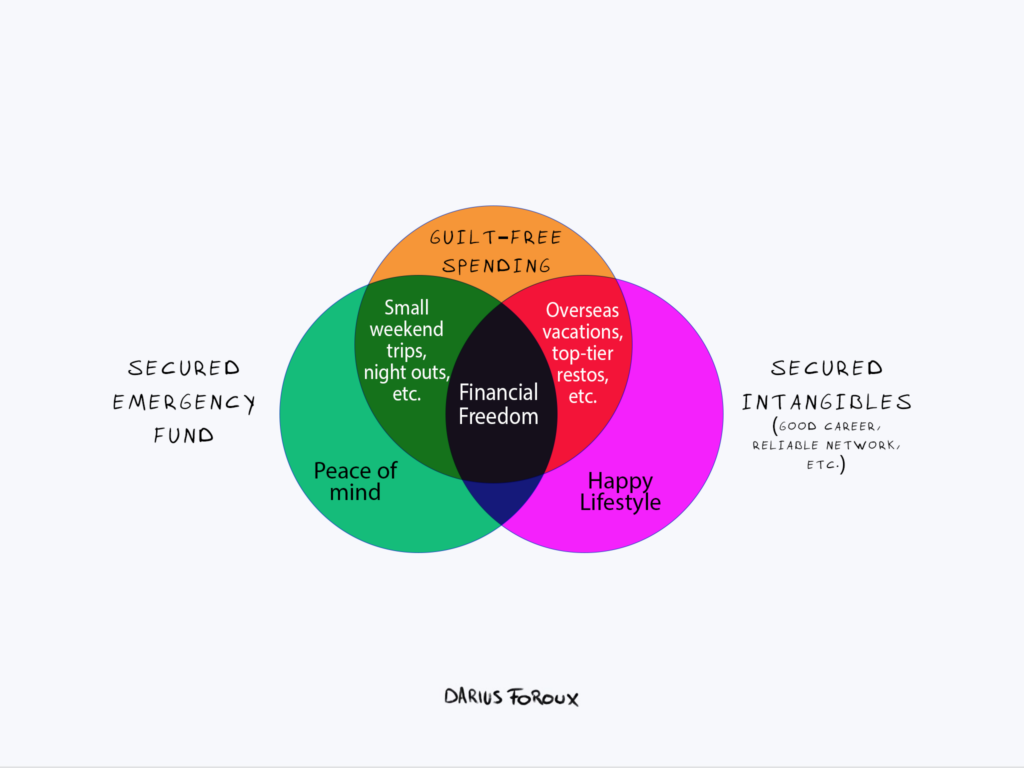

Level 1: The emergency fund

I think this is the most important financial foundation every person needs.

Build your emergency fund first, before buying anything big that’s mainly for pleasure (major electronic purchases, overseas vacations, etc.)

56% of Americans can’t even pay a $1000 emergency out of pocket.1Source: CNBC So try to at least have enough in your savings for when you suddenly need to pay an emergency expense.

This doesn’t mean you have to be overly frugal and deprive yourself of everything. Some people end up splurging as a result, which messes up their finances even more. To avoid that, you can focus on giving yourself milestones with your emergency fund. It can look like this:

- 1-month emergency fund — Have enough in your savings to cover a month’s worth of living expenses. Depending on your income, you can finish this in a shorter period. Having a month’s expenses saved gives you peace of mind. Then, you can reward yourself with something small. Like an inexpensive drive to the mountains or a nearby beach. Or a budgeted night out with loved ones.

- 3-month emergency fund — You can have a bit more leeway to spend at this point. But remember to only buy things that actually matter to you. Too many folks spend money out of boredom. Try not to be one of them.

- 6-month emergency fund — This is the ideal emergency fund. You can suddenly lose your job and still have enough time to find a new one. Once you reach this, you can start saving money for bigger purchases, like that dream vacation you’ve been planning for a while.

Look, unless you have established multiple income streams that help you earn a healthy 6-figure income, building an emergency fund takes a lot of time.

During that period, you also need to live your life. The key is to balance saving while still doing things that give you joy.

Level 2: The intangibles of a secure, happy life

There are things that help us know we’re on the right track with our finances. Like buying a house, growing a retirement fund, and having a consistent investing strategy to leverage stock market growth, among others.

But there are also intangible things that can threaten your lifestyle if you don’t pay attention to them.

For example: Are you in a career you enjoy and want to work on for the next 10 years? Your career occupies a large chunk of your life. If you’re working a job you hate just to pay the bills and build your savings — then no amount of luxury goods would make you genuinely happy.

Dragging yourself to work every day just to afford a few weeks in the Caribbean is not the best way to live.

Another thing: Do you have a reliable professional network? I’ve talked about what I would do if my net worth suddenly dropped to zero; which is to utilize my network to get a job.

In an uncertain world, knowing the right people who can give you a job when you suddenly need it can provide peace of mind. A reliable professional network can also help you grow your life and career more, compared to what you can do all on your own.

As the old saying goes:

“If you want to go fast, go alone. If you want to go far, go together.”

This is why the most successful people in the world are not one-man shows (even if some of them want to make that impression). They always have a team of assistants, experts, and other professionals behind them.

Just look at the biggest, best-selling books in the world. Or the highest-grossing films. Or the most successful businesses. All of them are backed by big institutions.

A reliable professional network takes time and attention to build. This means having the balance between simply earning enough to buy expensive stuff guilt-free and providing value to people who can advance your life and career in the future.

Determine your financial independence number

To keep things even simpler: Know how much you need to be financially free.

Once you know your “financial independence number,” you can pace yourself accordingly.

A good rule of thumb: If you’re halfway through your financial independence number, and you have both levels 1 and 2 established — then you can pretty much enjoy your money more. Becoming overly frugal at this point will just make you miserable.

Again, life is uncertain. Try not to be the person who can’t buy things guilt-free. Or the folks who burn through their savings like there’s no tomorrow.

It’s all about balance. Save enough to live comfortably. But live in the moment every single day.