I used to be very bad when it came to personal finance. I didn’t even use a savings account until my late twenties. Sure, I had one, but I just left all the cash I had in my checking account.

That’s the best strategy for going broke. You either spend your money on stuff you don’t need, or you get lured in by speculative investments like Bitcoin, Gamestop, silver, cannabis companies, or whatever CNBC and the r/wallstreetbets guys talk about (yes, I actually used these opposites in the same sentence).

Anyway, if you’re going nuts because of all of the confusing financial advice out there; this article is for you.

The goal of this guide is to help you get more control over your personal finances. I will share proven strategies and methods that people use not only to manage their money but also to generate more money.

Content Of This Guide

- What Is Personal Finance? A Definition

- The 4 Phases Of Personal Finance

- The 3 Account Strategy For Saving More Money

- 5 Ways To Get Out Of Debt

- When To Take On Debt

- Ways To Make More Money

- A Stoic Way To Invest Your Money

- Best Personal Finance Books

What Is Personal Finance? A Definition

Personal finance is the activity of managing your own money. It’s about how much you spend, save, get into debt, and invest.

The way you manage your money depends on many different things. Age, education, ambition, family, country of residence, all play a role in your personal finance strategy.

While this guide will give you enough input to create a strategy, you must always look at your personal situation. It’s called personal finance for a reason.

What might work for a 21-year-old who’s looking at the stock market like a casino will obviously not work for my father, who’s in his sixties. This is obvious. The reason I mention this is because so many of us compare our financial situation with others.

The only person you should look at is yourself. How others manage their money is insignificant.

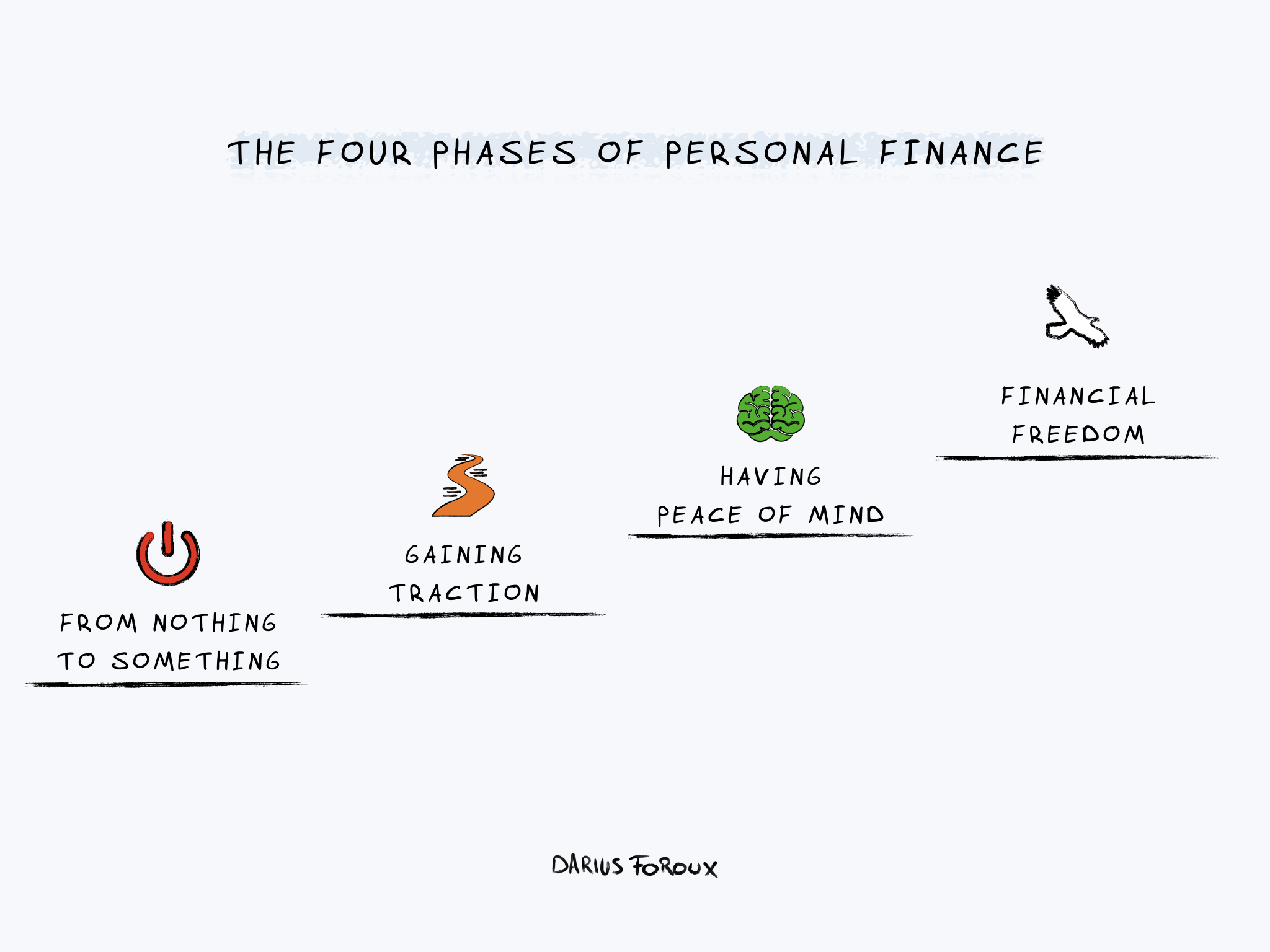

The 4 Phases Of Personal Finance

There are stages to personal finance. It’s good to have an understanding of where you are right now because every phase requires a different strategy.

Phase 1: From Nothing To Something

This is when you’re living from paycheck to paycheck, without having any savings. When I was at this stage, I did whatever it took to save at least one month of expenses. I worked more, and I saved more.

When you’re at this stage, I wouldn’t worry about anything else but building a financial buffer. Just save as much as you possibly can. It’s okay to be stingy when you’re in this phase. Your future self will thank you for it.

Phase 2: Gaining Traction

So once you’ve saved at least one month of expenses, you’re no longer living with a huge burden of looming bills. But you’re just getting started.

Once you’ve saved up at least one month of expenses, aim for saving six months of expenses. During this time you can relax more and spend some money on yourself. But never save less than 30% during this phase. It’s important to quickly get to a nice cushion.

Phase 3: Having Peace Of Mind

So you’ve saved at least six months of expenses. Now, put it away in a savings account and don’t touch it. Everything you save from now on is meant for investing. Remember that you don’t need to think about investing your money until you’ve got that six months of expenses.

Slowly dip your toe into some investments (more on that later). Phase 3 is all about making sure you stop the financial bleeding. When you experience net monthly financial growth, you’re on your way to more financial freedom.

Phase 4: Financial Freedom

In this phase, you have enough cash and investments to cover your cost of living. In the beginning, you can make huge leaps if you go from nothing to something. Most people accept the status quo when they are comfortable. It’s not a bad position.

You have enough cash to buy small things or go on vacations. But you still need to work. In phase 4, you don’t need to do anything.

We all want to get there. But if you’re in Phase 1-3, your focus is to build your personal finance foundation.

Too often, people are obsessed with personal finance. They read about it every day, look at their spending multiple times a day, and freak out when they have to spend their cash on something big.

That means money controls your life more than you think. If you’re reading this article, I assume that’s the last thing you want.

The 3 Account Strategy For Saving More Money

I have three bank accounts. Why not one? When you use one account for everything, it’s difficult to get a grip on your finances. And when you don’t have a grip, it’s difficult to save and invest.

That’s why I’m a proponent of three bank accounts. It systemizes my finances. Here’s how I use my accounts:

1. The normal checking account

My rule is to always keep less than $800 in this account. The amount of money you want to keep in your checking account depends on your personal circumstances. But I only use this account to cover groceries and other small purchases. That’s all I use my checking account for.

This makes it difficult for me to make big purchases. Every time I want to buy something that’s more than several hundred dollars, I need to transfer money from my savings account. Guess what happens? I think to myself, “It’s not worth it.” That’s how I’ve saved myself from buying a lot of crap.

2. The fixed costs account

I created a separate bank account for my fixed costs and always make sure there’s enough money in that account to cover my mortgage and bills for six months.

I don’t use this account for anything else. This also gives you a clear view of how much your cost of living is.

Most banks allow you to have multiple accounts at no additional cost. You don’t even need an ATM card for your fixed costs account. You’re not making physical payments with it. Simply set up a direct debit so you don’t have to worry about making the payments manually.

3. The savings account

I’ve set up an automatic payment that wires a set amount every month to my savings account. This way, I’m saving the same amount every month.

If you stick to your rules, pay your fixed costs first, and wire cash to your savings account, you can spend what’s left in your checking account.

Most people do the opposite. They spend their income first and then try to pay the bills with what’s left. And if there’s something left, they’ll save it. To become wealthy, you want to save first, and then spend what’s left.

5 Ways To Get Out Of Debt

Can you save money when you’re in debt? Should you put all your savings into paying off your debt? Which debt should you pay off first?

I personally like to have savings, regardless of debt. So I never spent all my savings on paying off debt when I had it. But how do you start getting out of debt in the first place? Here are 5 steps to do it right.

1. Do a personal finance assessment

Getting out of debt is just like any goal; You need to know where you are, to see where you’re going. Here are the factors to assess your financial health. Look at your money from the most simplistic point of view by asking:

- What’s coming in?

- What’s going out? And where’s it going?

- What’s left?

That’s all you need to know. If you don’t know where your money goes, you can’t manage it. Becoming aware of your financial health will help you to create a base level. Aim for going up from here.

2. Negotiate lower interest rates

This doesn’t work with all creditors, but it’s worth a try because it can be a quick win. If you can negotiate a lower rate, you will decrease your fixed costs instantly.

But creditors will probably not reach out to you and say, “Do you want us to decrease your interest rate?” You have to proactively reach out to your bank or credit card company directly to make something happen.

There are a lot of tips on the internet about negotiating lower rates. But I would keep it simple. Call a company up and be honest about what you want and why.

If the call center agent is an idiot, hang up and try again a week later. The amount of help you get depends on the person you speak with.

3. Make extra payments

Maybe you’re doing well with your business or freelance work, and money is coming your way. Or maybe you’re receiving a holiday bonus. Whatever it is, this is a great opportunity to make extra payments on your loans.

I like to start paying off the loan with the highest interest rate first because that makes the most sense to me. Others like to start with the smallest loan and pay it off quickly so they feel like they’re winning.

The truth is you only win when you’re out of bad debt. So whether you go left or right, your goal is to end up at the same destination.

4. Temporarily live on a budget

I’m not a fan of budgets. I’ve talked about how excessive budgeting won’t make you rich, and that it places you in a scarcity mindset. But a temporary budget is necessary if your debts are overwhelming.

We all go through winters in our careers. Sometimes we just have less to spend. In those cases, it’s good to set a budget and stick to it. Keep reminding yourself this is temporary. When you’re financial situation looks better, get rid of that budget and simply live below your means based on your gut feeling. There’s no need to defend every penny you spend.

5. Cancel unnecessary memberships and habits

Regardless of budget, do you really need to have 10 different subscriptions for entertainment? Netflix, Hulu, YouTube, Apple Music, Spotify, and so forth. Just get rid of most of them.

I still don’t take too many subscriptions because I want to manage my desires. I only pay for Netflix, Prime, and Apple Music. And we share it with my family.

Make a list of all your memberships and subscriptions and cancel everything you don’t need. The best way to save money is to desire less.

When To Take On Debt

Once you’re out of debt, you want to stay out of debt. At least, when it comes to certain types of debt. I stay away from credit card debt, personal loans, car payments, or any type of payment plan for consumer goods.

Avoid taking on debt for purchasing anything that does not increase in value over time.

Debt is a liability unless you use it to finance income-generating assets. The most straightforward example is buying real estate as a rental property. Another example is taking on debt to invest in your business.

I also see student loans as a form of investing, which can be a good form of debt. But there are limits. Is it worth it to take on $200K in student loans when you have cheaper options? That’s up to every person to decide. I do think there’s a lot of value in education.

Taking on debt is not a must. It’s a personal decision.

Getting a mortgage to buy a home that you will live in is not necessarily an investment. When you live in the home, it’s not generating any profit, and you can’t always count on appreciation in value.

But sometimes, it’s cheaper to buy than to rent. In those cases, it’s actually good debt. It all depends on where you live.

Ways To Make More Money

I never want to rely on one source of income. That’s too risky. When you only rely on your salary, you will have no income if you’re out of a job. It’s the same if you run a business or have a freelancing career.

Another reason I pursue multiple income streams is that it challenges me to become a better person. When you challenge yourself to provide more value, you will learn new skills along the way. That keeps life exciting.

So if you’re only relying on one income stream, I challenge you to explore all the different ways you can generate extra income. Here are a few ideas:

- Start a web-shop—Sell something you use yourself.

- Write and publish a “how-to” book—Write a book about something you know.

- Create a product in 48 hours—If you want to create a product, give yourself this limitation: What product can I design and produce within 2 days? You will immediately eliminate 99% of business ideas. Now, only focus on the things you can easily create and sell.

- Buy and sell objects you know a lot about—Buying and selling is the easiest way you can generate cash and help people get what they want.

- Build an app—If you’re a programmer, why not build something yourself? Try to find ways to generate income without trading your time for money.

If you’re looking for more, here’s my article with 8 ideas for online businesses.

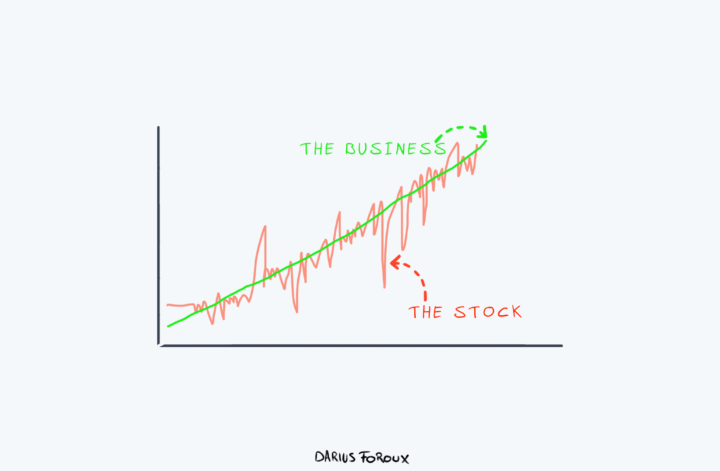

A Stoic Way To Invest Your Money

Unless you’re pursuing a full-time career in investing, the purpose of investing is not to make money at first. Too often we assume we can instantly make passive income by investing our money. But where does that initial money come from? You can borrow money, but that always comes at a price.

Investing is about creating long-term wealth. It’s an essential part of your personal finance strategy.

First, you manage the money you have, and then you use your money to generate more of it.

That’s how you build wealth. At least, this is the most responsible strategy. And it’s the strategy I pursue. I didn’t seriously think about investing until I was out of debt and had multiple ways of generating income.

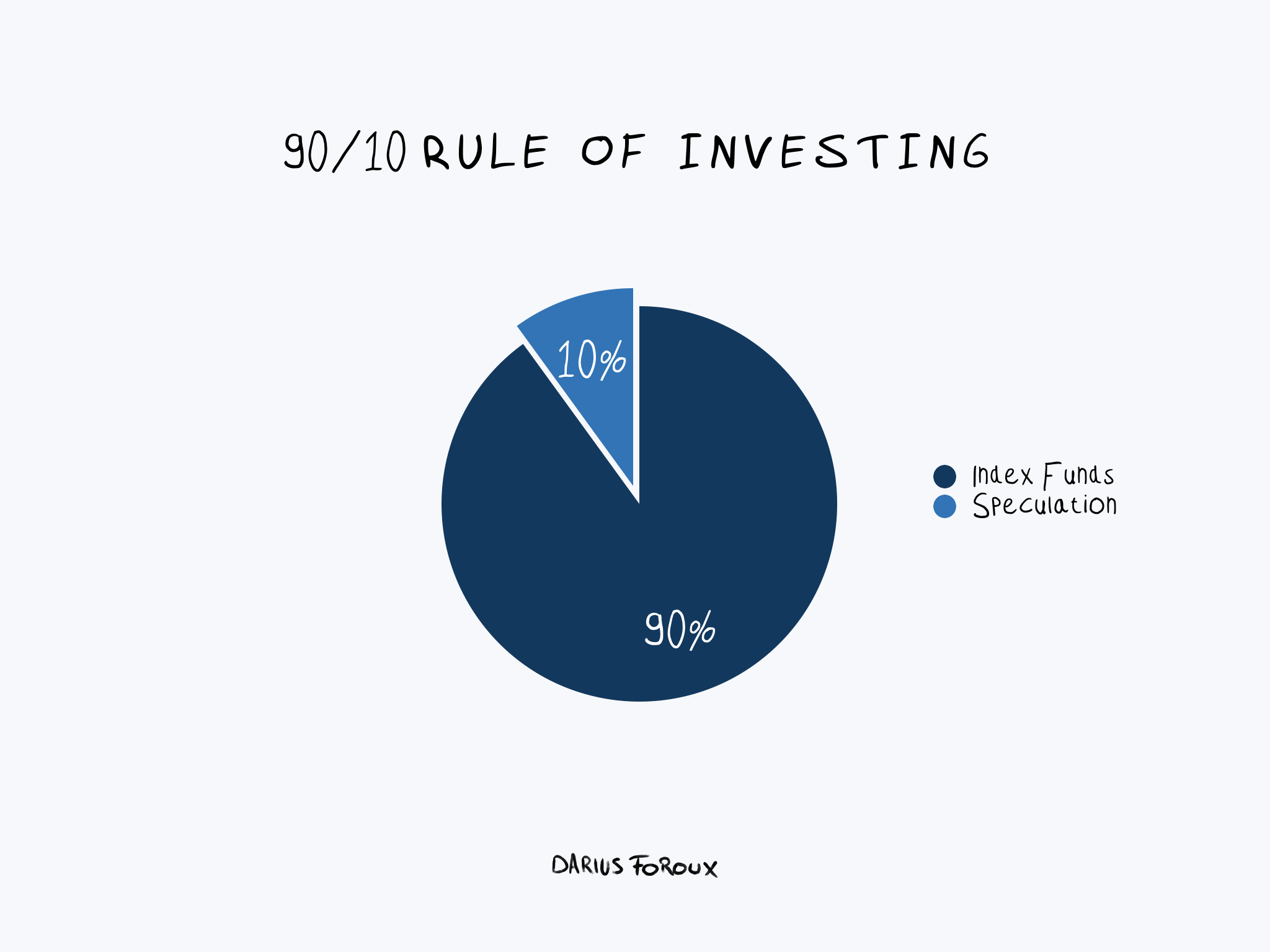

Right now, my investments are in real estate and stocks. I use the 90/10 rule, which is inspired by Stoic philosophy.

That means I put 90% of the money I dedicate to stocks in the Vanguard S&P500 index fund. No bonds or other index funds, especially after the COVID-19 pandemic, with interest rates at historically low levels.

And I use 10% to make a few bets on things I think will take off.

What type of investments fits best with your personality? If you can answer that, you’re more likely to stick with a winning strategy.

One of my friends only invests in commercial real estate. Another friend hates real estate because it takes time to look at properties, get funding, and manage the property. He prefers index funds and bonds. Both do well.

Investing is like philosophy. There are a lot of philosophies and there’s no right or wrong way to invest as long as you’re achieving results. No matter what you do, make sure you do something that’s a good fit.

Most of us waste too much time and energy pursuing opportunities that are not the right fit in the first place. For instance, stock options make no sense to me because I’m too risk-averse. Learning more about that is a waste of time for me.

Not sure if you’re ready to invest? Here are my thoughts on that.

Best Personal Finance Books

There are a lot of good personal finance books. I’ve read most of the books that are considered classic. Here are my three favorites.

The Richest Man In Babylon by George S. Clason

This book was published in 1926 and as far as I can tell, it was the first popular book on personal finance. The message of the book comes down to this: Rich people are rich because they save their money, don’t get in debt, and don’t spend their money foolishly.

The main message of the book is that you only get rich by paying yourself first. It’s a great book if you’re looking for changing your mindset.

Your Money Or Your Life by Vicki Robin and Joe Dominguez

What I enjoyed most about this book is that it teaches you to transform your relationship with money. This will change your life. Money is something you trade your life energy for. Think about it. You work to earn money.

More money is especially not better if you have to put your own well-being on the line. It’s never worth it. This book helps with realizing that.

The Little Book of Common Sense Investing by Jack Bogle

If you’re interested in index funds, you’ll love this book. Jack Bogle revolutionized passive investing. He founded Vanguard and created index funds.

Instead of buying individual stocks, Jack Bogle demonstrated that it’s much better to buy all the stocks in a certain index, industry, group, or even country.

History has shown us that indexing outperforms the majority of mutual funds. Plus, the fees of index funds are lower because they don’t have managers or expensive offices.

Be The Boss Of Your Money

Personal finance is all about expectations. For example, I don’t expect to never work again in my life.

I know that the FIRE community is all about early retirement, but that never attracted me. I simply want to do work that I enjoy doing. The idea of retiring and traveling is meaningless to me.

To me, it’s about making sure I’m the boss of my money and not the other way around. And I hope this guide has helped you to do the same.