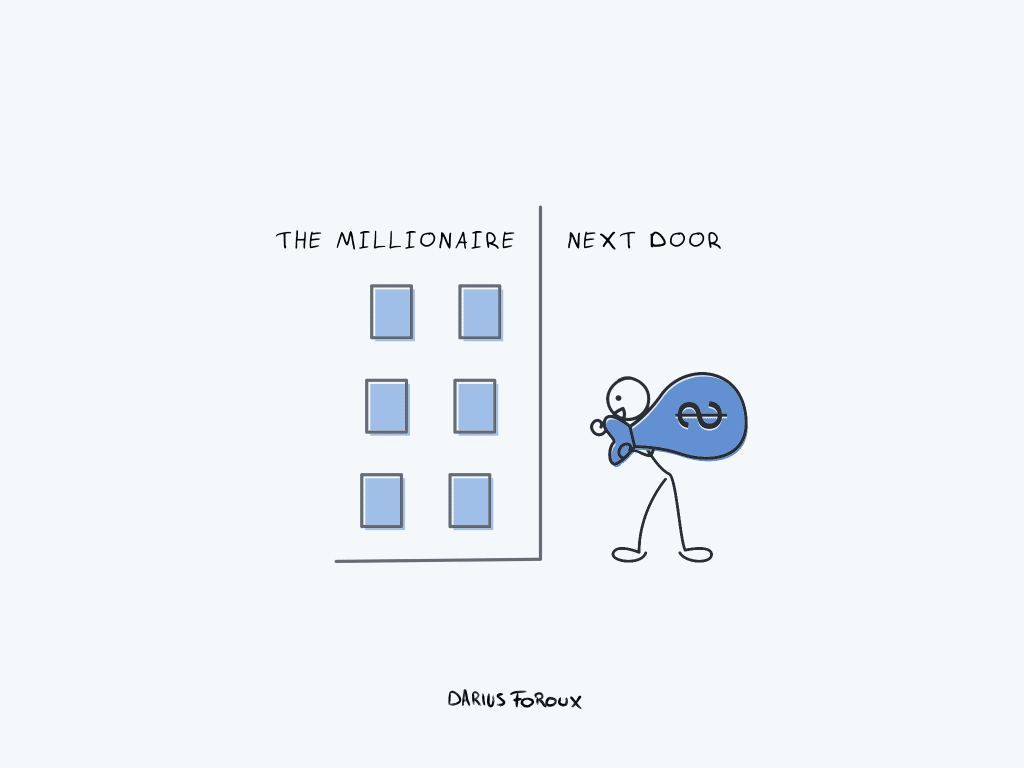

When researcher Thomas Stanley tried to learn how people became wealthy, he started by visiting upscale neighborhoods across America.

He discovered that many people who lived in expensive homes didn’t have much wealth. Instead, each millionaire he found didn’t look like a millionaire.

- They lived in middle-class neighborhoods, instead of “upscale addresses”

- They didn’t own the latest model cars or expensive watches

- They didn’t wear luxury clothing brands

- and so forth.

Stanley also expected most wealthy people to be descendants of old-money families, like the Rockefellers and Vanderbilts. But that wasn’t the case. Instead, he found ordinary people who built their wealth by themselves, in one generation.

His insights led him to write the bestselling book, The Millionaire Next Door. The book’s findings were simple but powerful:

“We discovered who the wealthy really are and who they are not. And, most important, we have determined how ordinary people can become wealthy.”

A lot of people confuse wealth with income. Wealth is not income. Even if you have a high income, spending it all means you won’t get wealthy. It’s all about living a fulfilling lifestyle you want below your means.

I used to have goals like, “I’d like to make a million dollars a year!” But that’s too dependent on outcomes. It gets you trapped in a cycle of chasing after more and more. And more money doesn’t lead to financial independence.

Here are the 5 steps you can take to build wealth and eventually become a “millionaire next door.”

1. Pick the right profession

Stanley identifies several professions in his book that would potentially earn well in the long term. But the most important aspect of a “right” career is a job that won’t become extinct in the future.

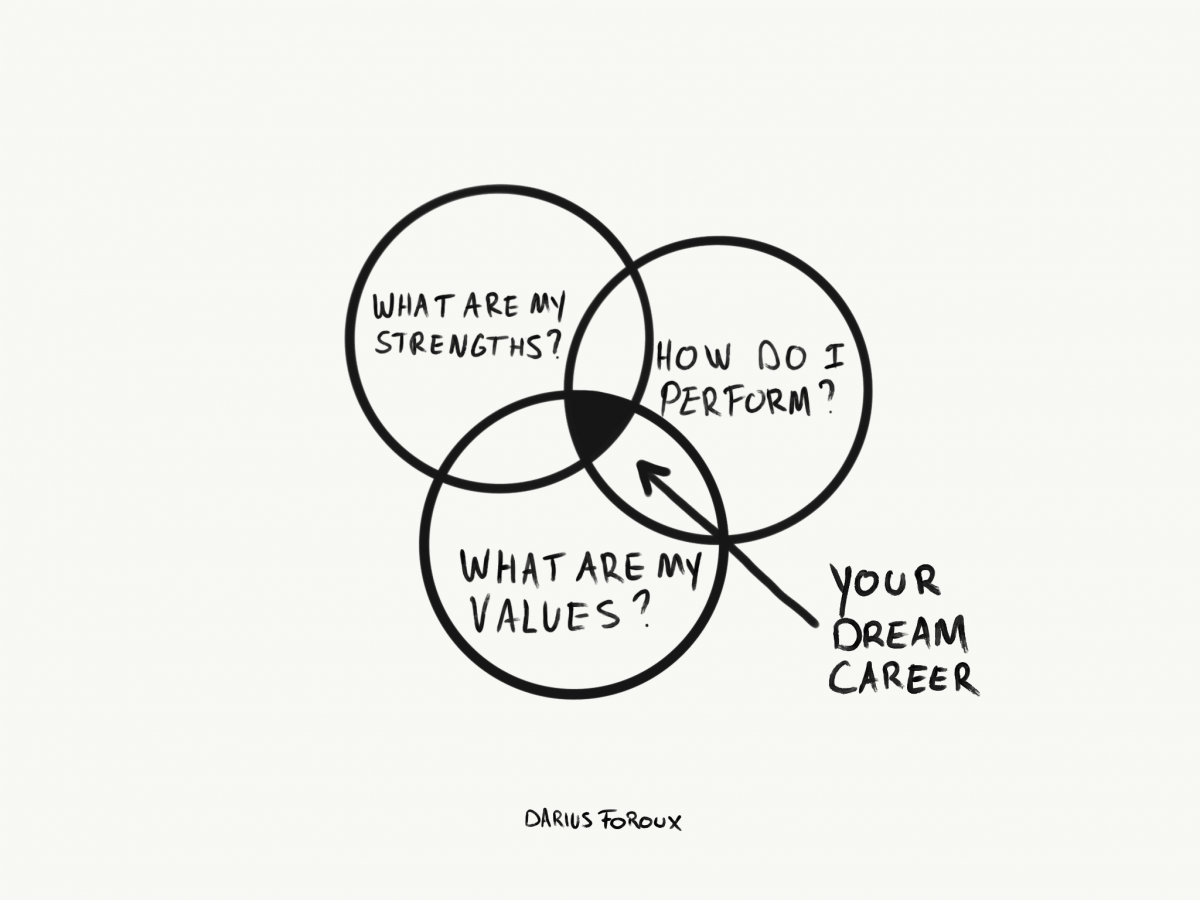

That aside, choosing a career path simply because it won’t go extinct isn’t enough. I used to ask myself these three questions when I was trying to figure out my dream career:

What are my strengths? — As Peter Drucker said, “Put yourself where your strengths can produce results.” The best product/service providers get the best deals and income. So figure out your strengths and focus on improving them.

How do I perform? — How do you get things done? How do you learn? Do you perform well under stress? Do you work well in large teams? Do you work better at a small company or a big one? How do you focus?

What are my values? — Know your non-negotiables. That’s how you can perform your best. Try to avoid doing something you don’t believe in, or working for a company whose values contrast yours.

2. Control your income by having options

The pandemic has shown us that having a single income stream is too unstable. Just ask those restaurant owners who closed for months during the lockdowns. Or those employees who were let go.

Multiple income streams give us options. And options provide us with freedom and peace of mind. That doesn’t mean you need to own many businesses or work 5 side hustles.

Especially when you’re just starting, having income-generating skills is more important. Wealth isn’t about having a high income. Here’s the most common definition of wealth:

“Wealth is a plentiful supply of a particular desirable thing.”

We gain wealth by providing value to others. When I talk about providing value, I’m talking about helping people professionally. When you can give a product or service that others find “desirable,” you don’t have to fear losing money.

Try not to be over-dependent on a single income source. That’s how you have more control over your income.

3. Don’t let outcomes dictate your desires

If you’ve been following my blog for a while, you’ll notice I’m not a fan of social media. That’s because most content there is entertainment. And not the best place to learn things. But people sometimes confuse that.

Take those social media finance gurus, for example. You see these people talk about investing or starting your own business while sipping mojitos in the Caribbean. But making money doesn’t need to be instagrammable.

That’s why I avoid inflated numbers when I talk about wealth. Things like:

- “Will a six-figure salary make me financially independent?”

- “If I have ten million bucks by age 45, can I retire early?”

- “When I’m earning a million bucks a year, will I finally be satisfied?”

Having specific goals is fine. But try not to get too attached to outcomes.

For example, whether or not your business or job will earn you six figures in a few years is not entirely within your control. You can only control what you do and how you react to things.

4. Invest after you save

As of May 2022, Gallup found that around 38% of Americans who earn between $40,000 to $99,000 a year — while 75% of households that earn less than $40K — don’t have stock market investments.1Source: Gallup News

I assume the ratio of people who don’t have money in the stock market is even higher in other countries. After all, over 45% of adults around the globe aren’t capable of paying out of pocket for an emergency.2Source: WeForum.org

That means most people are not benefiting from the power of compounding. And they’re not leveraging the long-term growth of the market.

For people living paycheck-to-paycheck, the first priority is to build an emergency fund. Even just enough to cover a whole month’s expense. It’s best to start small, then aim for 6-months’ worth of expenses.

When you have half a year of expenses safely tucked in a savings account, then you can slowly dip your toes into investing. And the key to investing is this: Avoid investments you don’t understand. That’s how you prevent losing all your money.

Instead, keep a simple investing strategy that will help you build sustainable wealth in the long term.

5. Have a partner with the same values

One of Warren Buffett’s pieces of advice on becoming wealthy has nothing to do with money. In a conversation with Bill Gates at Columbia University, about building wealth, Buffett said:3Source: Gates Notes

“It’s important to associate with people that are better than yourself and actually the most important decision many of you will make, not all of you, will be the spouse you choose. And you really want to associate with people who are the kind of person you’d like to be.

You’ll move in that direction. And the most important person by far in that respect is your spouse. I can’t overemphasize how important that is.”

It’s no surprise The Millionaire Next Door data reports that most frugal millionaires have married spouses who are also frugal themselves. This avoids two things.

First, one doesn’t get stuck with a spouse who wastes all the money. Because it doesn’t matter how frugal or wealthy a person is if their spouse spends it all.

And people can prevent one of the top reasons why married couples fight: money.4Source: Investopedia When you partner with someone who has the same money mindset, you’re less likely to have financial disagreements.

Lifestyle matters

Stanley and his team once booked a high-end, luxury suite with an expensive buffet to accommodate their millionaire interviewee. When the interviewee arrived, he ignored the expensive wines and foie gras.

He said he only drank “scotch and two kinds of beer: Budweiser and Free!”

That doesn’t mean you shouldn’t buy expensive wines or foie gras if you genuinely enjoy them. What matters is to live simply most of the time.

Always avoid peer pressure to dictate what you do and how you live your life. The whole idea of being a millionaire next door is that no one knows about your wealth.

You do it for yourself, family, and the people who matter to you. To me, that’s the most honorable reason to build wealth.