When investors deal with an unusual event, they often say, ”This time it’s different.”

It often happens during the formation of bubbles. For example, in 2021, several investors and commentators said we were in a bubble for growth stocks and SPACs.

Some said it was very similar to the Dotcom crash of 2000. But many investors said, “No, it’s not like that. Back then, companies didn’t have any earnings at all. This time, the companies have good revenues. Sure, the prices might be high, but we’re certainly not in a bubble.”

We were. And it slowly started to burst from mid-2021. One thing to remember is that not all bubbles come to a grinding halt.

Didier Sornette, a former professor of Entrepreneurial Risks at the Swiss Federal Institute of Technology, did extensive research on stock market bubbles.

He published a book about it called, Why Stock Markets Crash. Sornette found that between half to two-thirds of all bubbles crashed.1Source: WSJ

Others simply faded over time, something similar to what happened with SPACs and other Covid-19-related assets that were popular.

The reality is that stock market events repeat themselves. When fiscal policy is easy and credit comes cheap, asset prices rise. And at some point, that trend reverses. There’s no “This time it’s different.”

I get the pull of a bubble. I’ve been there too. Sometimes it seems the market can only go up. But we all know that has never happened in history.

There are many other fallacies and thinking errors when it comes to investing. Here are two others you’ll want to keep in mind if you don’t want to lose your investments.

The “Hot hand” fallacy: When you can’t lose

I’ve been an NBA fan since I was a child. One of the main ideas in basketball is that players sometimes can get a “hot hand.”

I also experienced this when I played basketball in high school. I remember one game when I had 40 points. That season, I was a backup center and I averaged around 8 points a game.

But one game, I couldn’t miss. It started the moment I was subbed into the game. All my shots went in. My teammates started to cheer me on. Then, my coach left me in the game. And I just kept scoring on the other team.

I felt like Shaquille O’Neal for one game because that was how long my “hot-hand” lasted. After that game, I reverted back to my scoring average.

When you invest during a bull market, you can quickly get the idea you have a hot hand. You feel like a winner on every investment or trade. Nothing seems to go wrong.

As they say, during bull markets everybody is a genius…Until they’re not.

The “hot hand” fallacy is a cognitive bias that assumes a person who experiences a successful outcome has a greater chance of success in further attempts.

While I do believe in the power of momentum, I also believe that everything and everybody reverts to the mean.

- When Lebron James makes 4 out of 5 three-pointers one game, he will probably make 2 out of 5 (which is roughly his average over his career) during others.

- When a stock outperforms the market for 5 years, its growth will likely match the pace of the overall market in the following 5.

While hot streaks certainly happen, they never last. Relying on streaks is simply not sustainable if you want to build long-term wealth.

The “Over-extrapolation” fallacy: The future is not the same

Extrapolation is the act of estimating the values of a variable based on known data. Generally, this means that observed trends are extended.

For example, scientists can look at the existing birthrate and use that data to extrapolate the future population. Often, they get it right. Extrapolation works well in many fields like demographics or physics. But it’s not a reliable method when dealing with finance and the economy.

Many people tend to extrapolate present economic conditions into the future. That always leads to having a future perspective that’s the extreme of today.

- If today is bad, you assume that the future will be even worse. You extrapolate the downward trend.

- If today is great, you assume the future will be even greater. You extrapolate the upward trend into infinity.

This “over-extrapolation” fallacy is responsible for investing more during bubbles and pulling out of the market during crashes.

Imagine you were investing in 2008 and you were extrapolating the present. You assumed that banks would be in trouble forever, the recession to turn into a depression, and that home prices would keep going down.

But that’s not the case now.

When you observe trends, you notice they usually reverse at some point in time. As the adage goes: “Nothing lasts forever.” That’s true for both the good times and the bad.

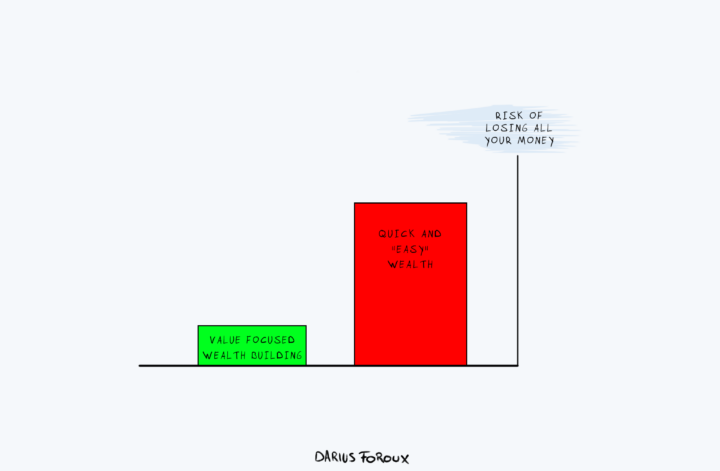

The aware investor avoids losing all their money

Long-term investing is not about picking the right stocks, taking risks, buying low, or selling high. It’s about making sure you can keep investing.

Smart investors stay in the game, no matter what the conditions are. They recognize patterns in the market, but more importantly, they can recognize patterns in their own thinking.

When you can do the latter better than others, you automatically have an advantage because you can correct your own behavior. That’s an important characteristic of sound investing.

You even don’t need to know everything.

When you’re aware of the three biases in this article, you’re already ahead.